We entered 2022 expecting that the U.S. agriculture would face a mixed outlook, due to a combination of escalating costs, supply chain bottlenecks, and high energy prices. While the prediction rang true, the year proved even more tumultuous given Russia’s invasion into Ukraine, 40+ year high inflation levels, and a steep economic slowdown in China.

Beyond this, the Federal Reserve raised interest rates at an unprecedented rate to finish the year at 4.25% to 4.50%, and the crypto currency space imploded. Interestingly, agricultural cooperatives and independent ag retailers generally delivered above-average results driven by agronomy related sales and services, even in the wake of fertilizer and chemical supply chain disruptions.

Ag Retailers in the U.S. delivered exceptionally strong results during 2022 even in the wake of supply chain disruptions

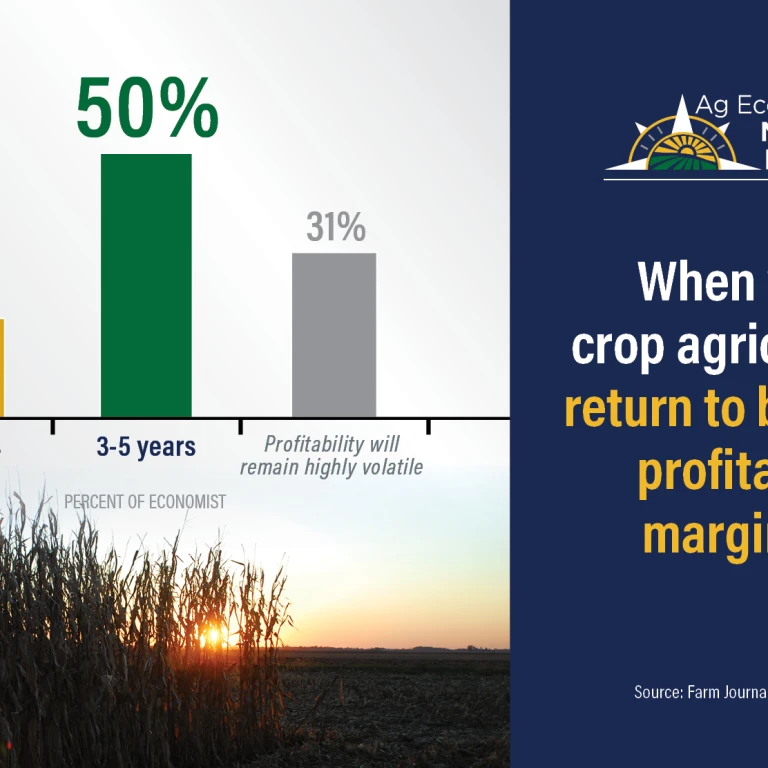

Looking forward to 2023, we see an environment of margin pressure amidst a slowing economy, higher interest rates, high labor and energy costs, and trade uncertainty with China and possibly Mexico. Ongoing drought and volatile weather remain additional risk factors for crop production. Animal feed demand is softening, reflecting flat overall growth in the domestic livestock sector.

Grain elevators and merchandisers will likely face a mixed picture for the year ahead. On the negative side, grain exports were stunted in Q4 2022 due to a combination of a strong U.S. dollar by transportation bottlenecks on the Mississippi River and reduced purchases of soybeans and corn by China, both of which could result in missed opportunities for the current marketing year.

And then there is the Mexico situation: The country’s president decreed during 4Q 2022 that Mexico would ban the importation of genetically modified corn in 2024, which would have jeopardized roughly one quarter of all U.S. corn exports. Subsequently, Mexico’s Secretary of Economy suggested the ban will be pushed back to 2025. We believe that the GMO corn debate is a bargaining tactic in Mexico’s quest to improve Mexico/U.S. energy trade policies.

On the positive side for U.S. producers, Ukrainian grain and oilseed production and exports are likely to remain constrained for the next few years due to the Russia conflict. This will provide underlying support for grain prices, and aid U.S. corn exports. Finally, combined global ending stocks for grain and oilseeds are still very tight after falling for four straight years to their lowest level since 2013/2014. It will take at least a couple of years to build stocks to a more comfortable level.

Ag retailers begin 2023 on strong financial footing but face several challenges. Labor shortages and rising wages will negatively impact margins. In addition, wholesale fertilizer acquisition costs will remain high during the first half of 2023 as cooperatives not only absorb high barge and rail costs but also compete with export markets for limited supply. Some 70% of European fertilizer production was offline during Q3 2022 as the region dealt with record-high natural gas (feedstock) prices. Fertilizer prices will likely begin and end 2023 at elevated levels, minimizing the opportunity for retailers to capture the same level of carry margin that was available during 2021/22.

The retailer of the future will be defined by their ability to service the famer of the future.

Looking beyond 2023, I will quote Brett Sciotto, the founder of Aimpoint Research: “the retailer of the future will be defined by their ability to service the famer of the future.”

Read Ken Zuckerberg’s “Ag Watchlist” for the week of Jan. 9

Kenneth Scott Zuckerberg is Lead Industry Analyst, Grains, Farm Supply & Biofuels, CoBank.